When I started to go down the crypto rabbit hole in 2018 and 2019, what originally got me interested was the potential for interoperability and efficiency. Rather than requiring intermediaries to trade a stock or exchange deposits between a bank, a shared ledger with cryptographic proofs could allow institutions and individuals to exchange value directly. Although it went nowhere at the time, I was fascinated by the Australian Stock Exchange’s DLT project with Digital Asset (see my b-school paper 😀). After this brief period of private and enterprise blockchain initiatives that largely fizzled out and were shelved, we lost the storyline a bit, but finally, we’re back.

As the GENIUS bill provides a framework for stablecoins to much great fanfare, the chatter around the term “tokenized deposits” is returning. After the passage of GENIUS, there has been much speculation and hype around banks launching their own stablecoins and almost every bank executive got asked about this during their Q2 earnings calls. Interestingly, the response has generally been some form of “…sure stablecoins are interesting, but tokenized deposits are where the real opportunity lies for banks.”

While a number of people have summarized Citibank’s CEO Jane Fraser’s Q2 remarks, I think it’s worth reading the transcript directly (found here). Fraser exhibits a grasp of stablecoins and their strategic (or not so strategic implications) that is quite impressive. She had clearly taken a look at (or been briefed) on the Visa stablecoin dashboard when she cited this stat: “…right now, stablecoin, about 88% of all stablecoin transactions are used to settle crypto trades. It’s only 6%, which is payments.”

Most importantly though, Fraser highlighted that tokenizing deposits are the real opportunity. The challenge today is that if I want to move money between the US and Hong Kong with stablecoins, I need to hop on and off a blockchain. This requires stitching together solutions, creates friction, and drives up transaction costs. Fraser again, “And in a traditional offering, if you are moving from cash to stablecoin and back to cash, right now, you’re incurring as much as a 7% transaction cost. I mean that’s just – that’s prohibitive.”

The 7% is a bit of an extreme example, but her point is right that if you are moving funds from one Citi account to another, it’s a superior way to move funds from New York to Hong Kong. Of course, the issue here is that we all are not going to transact on a private Citi ledger. There will need to be some interoperability. This is where things get interesting.

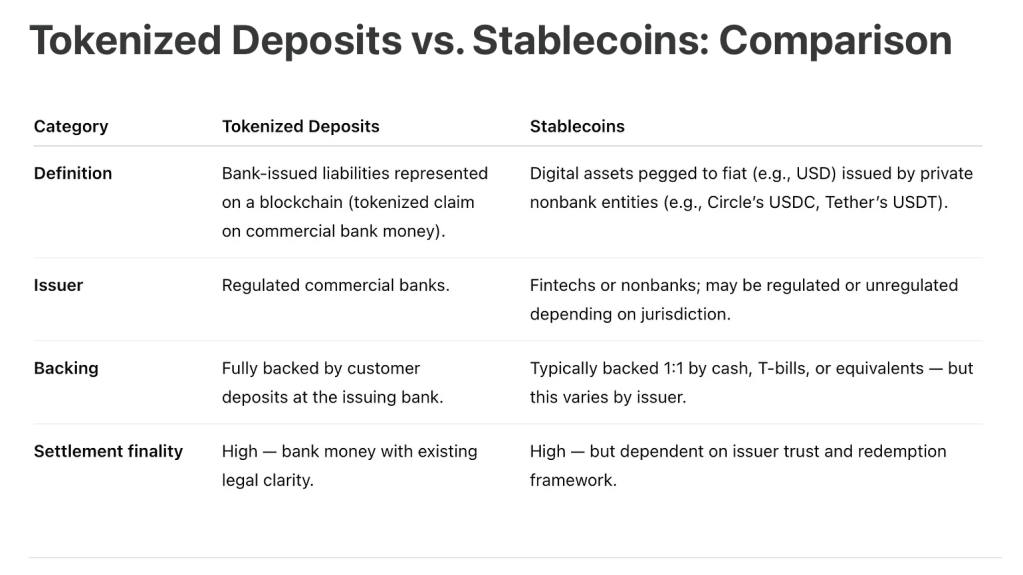

To back up though, I first want to define our terms. Shout out and credit to Rich Dooley for the chart below. I randomly came across his substack post on this topic and thought his chart was solid, so I am resharing here.

Rich’s article is worth checking out because he goes on to discuss the pros and cons of each. He is spot on that the main challenge facing tokenized deposits is interoperability. Tokenized deposits have distinct advantages, particularly from an issuers perspective. Since it is simply a representation of a $1 deposited at your bank, you do not need to hold reserves in a 1:1 ratio. You can put that capital to work more efficiently, by making commercial loans rather than solely investing in short term treasuries. At the moment, you don’t have to worry about the underlying stability of the peg whereas with a stablecoin you might. Of course, GENIUS is attempting to address this, but even USDC unpegged briefly in 2023.

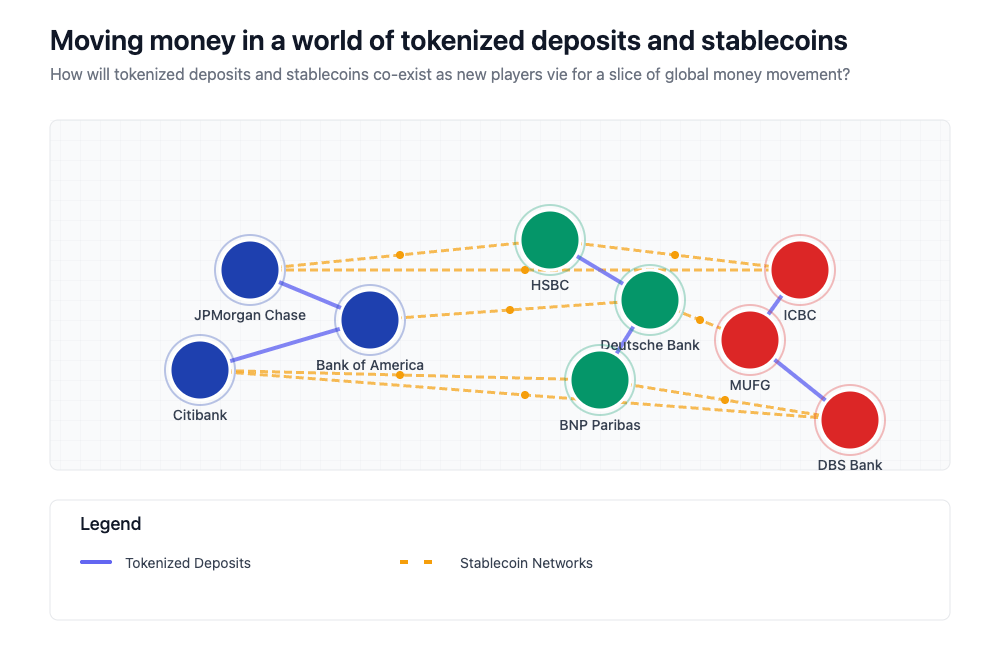

Really where I think tokenized deposits will shine and find a true use is in intra-bank and inter-bank settlement. Fraser was talking about intra-bank settlement in her press release, and she alluded to a potential collaboration between the major banks in the US. Rather than JPMC, BofA, and Citi issuing a joint stablecoin, I think it’s more likely they find better ways to exchange their own tokenized deposits within some sort of closed network. There is a true value proposition here. The Fed’s real time payment system is also addressing this challenge, but there is certainly efficiency and cost savings to be had if JPMC and Citi can immediately settle a transfer by moving tokenized deposits rather than relying on a batched settlement that cuts off at a certain time during the day.

You can imagine a world where Citi deposit tokens are exchanged amongst a few core banks, but what happens when you want to send that Citi token to Canara Bank in Bangalore, India (a state-owned bank that I worked with earlier in my career 😀). Is Canara going to accept those Citi deposit tokens and will Citi want its tokens custodied by banks all over the world. Simon Taylor got into this problem a bit on the Tokenized podcast. It’s not clear how this plays. How widely will tokenized deposits be used?

As I sit here in July 2025, there are still a lot of unknowns. I have a loosely held hypothesis that we might end up in a world of closed loop tokenized deposit consortiums that are then connected to the broader financial ecosystem via stablecoins.

To flesh this out, let’s go back to my Citi and Canara Bank example. Perhaps both institutions do not want to deal in Citi deposit tokens, but each institution is comfortable transacting in large cap stablecoins like USDC or USDT. No knock on Canara, but maybe Citi is not comfortable holding deposit tokens from foreign institutions, or vice versa. In any case, each of these banks will have access to USDC and USDT liquidity and will likely both have these stablecoins on balance sheet. When I go to send funds to India from the US, you could envision a world where my money at Citibank is in the form of tokenized deposits. Those Citi tokens are then swapped into USDC, sent to a Canara wallet address on Solana, and then the USDC is offramped into INR (or maybe it’s just swapped into a Canara token). This may sound far-fetched and still requires some real stitching together of systems, but this is one mental model for how I see tokenized deposits and stablecoins evolving and potentially co-existing.

It begs repeating that we need to ensure we don’t end up just designing a new global money movement model that is almost equally as complex as the correspondent banking system that is now used to move funds around the globe. I believe there is real innovation here that can help move money more efficiently and at lower cost, but it is going to require deeper thinking and more interconnection between the worlds of fiat and stablecoins. The major banks dominate the FX market today, and they can likely continue to play a huge role here even as upstarts like Circle and Tether challenge the existing model of cross-border money movement. Of course players like Circle want to become banks; they see the vast potential of tokenized deposits.

Leave a comment