The headlines keep coming on the theme of stablecoins converging with traditional finance. One of the more recent eye-brow raising announcements was Fiserv getting into the stablecoin game with FiUSD.

If you work in the financial services space, you have likely heard of Fiserv, but if you were asked what the company does, you may wave your hand and say they provide some type of financial infrastructure. So let’s start there. What does Fiserv actually do? What are their product offerings, and how do they generate revenue? From there, we can explore why they launched a stablecoin and what might come next.

Fiserv background

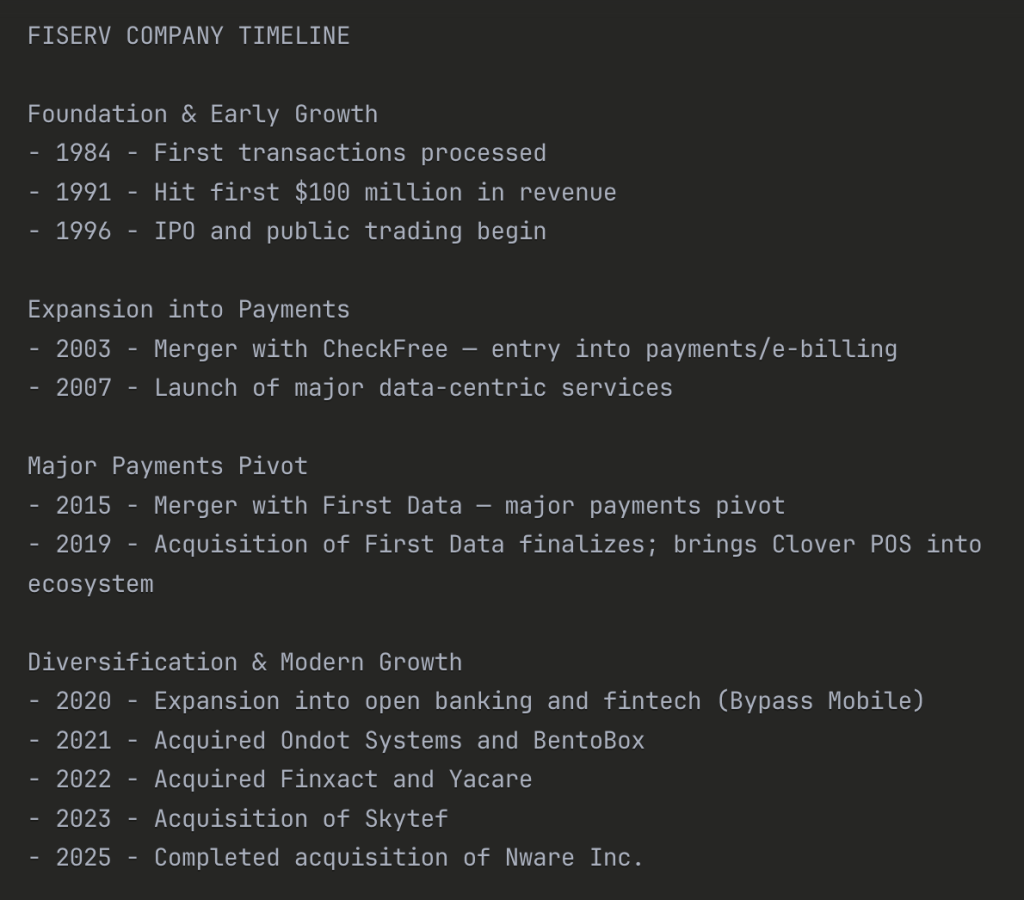

Fiserv was founded back in 1984 during the days when companies still went public relatively quickly. Within two years, the company was listed on the Nasdaq, and over the next several years sustained strong growth largely driven via acquisitions. This has been a theme at Fiserv that has continued to the present day.

Note: I tried to have ChatGPT create a pretty timeline of Fiserv’s acquisition history, but I gave up after this proved slightly too challenging.

In total, Fiserv has acquired 45 companies over its history, including 8 in the last 5 years. But what does Fiserv actually do? There are two core business segments at Fiserv: Core Banking and Merchant Solutions. Let’s start with Core Banking.

Core Banking (referred to as “Financial Solutions” in Fiserv’s reporting)

It’s a giveaway in the name, but a “core banking system” is the platform that enables the bank to run its main functions such as keeping track of customer deposits, interest payments, outstanding loans, transfers between accounts, and all the other functions we think of as banking.

For a variety of reasons, massive banks like JPMorgan Chase will have bespoke core banking solutions that they have partially developed in house and stitched together over years of acquisitions. For the majority of banking institutions though, they outsource the core banking architecture and use a provider like Fiserv. In the US, we have the “big three:” Fiserv, FIS, and Jack Henry. These three core banking software providers cover over 70% of the market. Fiserv is the market leader with 42% market share. This means that just about one in two banks in the US is running a Fiserv core.

In practice, Fiserv actually has a range of different core banking products. These range from more legacy solutions like DNA and Premier to their more recent cloud native solutions offered through the Finxact platform they acquired in 2022. In any case, what this means is that Fiserv is essential to functioning of thousands of US banks and many thousand more banks around the world. In addition to the banking core, Fiserv also offers a range of other add on banking services. If you’re a smaller regional bank, you do not have the resources that a JPMorgan Chase does to create a mobile banking platform. As a result, you might rely on an out of the box solution from a provider like Fiserv.

All told, the core banking unit generates about $10B annually in revenue for Fiserv. It’s a solid business with steady growth, particularly as digital payment options, like supporting Zelle, become a bigger part of the business. One thing I did not realize is that Fiserv provides infrastructure services that allow banks to support Zelle. As the ubiquity of Zelle grows that appears to help Fiserv’s bottom line.

Merchant services

The second major business unit within Fiserv is merchant services. This is a broad term that encompasses a variety of payments businesses that sit inside Fiserv. A big portion of this revenue came onboard with the acquisition of FirstData in 2019. Prior to that, Fiserv was primarily a core banking shop. Merchant services is now about a $9-10B annual revenue business for Fiserv. There seems to be a lot of growth opportunity here for Fiserv, particular on the SMB payments side.

One of Fiserv’s crown jewels is Clover – a point of sale payment solution with embedded financial services for merchants. Clover plays slightly upmarket from Square allowing Fiserv to capture payment flows from SMBs all the way up to enterprises. When you look at Fiserv’s Q1-2025 deck, you’ll notice that Clover revenue is up 27%. It is one of the key growth drivers within Fiserv.

All in all, when you look at the merchant services business at Fiserv, there seems to be a lot of room for growth, both organically and via acquisitions. The FirstData acquisition is still relatively recent, and I imagine the executive team sees a big opportunity to go deeper on payments while maintaining the company’s key position in the core banking market.

Why launch a stablecoin?

I spent all this time on background because I think it’s helpful to frame Fiserv’s decision to launch FiUSD. Yes, Fiserv is a core banking infrastructure company, but it is equally a payments company. Stablecoins are challenging the way that individuals and financial institutions move money. From supporting Zelle to enabling a merchant to accept a card at the point of sale, money movement is core to Fiserv’s business.

When you look at how Fiserv advertises its ability to support Zelle, it has trademarked the term “Turnkey Service for Zelle.” By launching FiUSD, Fiserv appears to be heading towards a similar strategy for stablecoins, a turnkey service to enable financial institutions to turn on stablecoin support. From there, you could easily see stablecoins becoming part of the Clover offering on the merchant services side. Clover is particularly strong in the hospitality sector. It’s still early, but we’re starting to see stablecoins as an important payment method for international travel. Do we see a stablecoin icon on the Clover payment option list sometime soon? I would think so.

All this is to say, Fiserv has a real incentive to at least understand what is happening in the stablecoin world and ensure it’s in the mix as the ecosystem grows. During an earnings call Jamie Dimon of JPMorgan Chase recently commented on stablecoins saying, “We’re going to be involved in both JPMorgan deposit coin and stablecoins to understand it, to be good at it. We don’t know exactly — I think they’re real, but I don’t know why you’d want a stablecoin as opposed to just payment.” It’s not the most glowing endorsement of a stablecoin strategy and Dimon has generally been highly skeptical of crypto and stablecoins, but I think the quote hits on a common line of thinking at traditional institutions.

It’s not 100% clear yet how stablecoins will be used, but there is a need to understand this technology. It has the potential to disrupt legacy businesses, but it can also open up new grow channels, particularly for infrastructure players like Fiserv. The Head of Embedded Finance and Digital Assets Product at Fiserv, Cooper Thompson touched on how stablecoins could have broader implications for a variety of business products:

“For us, stablecoins are the entry point. We see them as digital cash, a new money movement rail. But we’re not stopping there. Our broader strategy includes programmable payments, tokenized deposits, and real-world assets.”

I imagine we’ll get a bit more clarity on the Fiserv stablecoin strategy in the quarters ahead as FiUSD gets into market, and we see a bit more action around tokenized deposits.

What are the mechanics of FiUSD?

Let’s dive into how this Fiserv stablecoin will actually work. FiUSD is a USD-backed stablecoin that will be issued using a combination of Paxos and Circle’s technology. It’s still a bit fuzzy to me how exactly that technology partnership will work, but Paxos is obviously known for helping many big players like PayPal get into the stablecoin game with their issuance platform. FiUSD will initially be available on only Solana. This is a nice win for the Solana ecosystem as most institutional projects have tended to start with EVM first.

Internally, FiUSD will be available as part of Fiserv’s Finxact core processing platform. Finxact is a cloud banking ledger software that Fiserv bought a few years back. The value add of Finxact is that it helps modernize core banking infrastructure, so it’s exciting to see stablecoins becoming part of the modern core banking offering.

Another interesting note from the announcement is that Fiserv is partnering with PayPal and MasterCard as part of the FiUSD launch. Presumably this is for distribution to help get the stablecoin into the hands of more merchants and users.

Outstanding questions

There are a lot of outstanding questions related to this stablecoin. I jotted down a few that are top of mind for me. They are a mix of practical questions about the mechanics of the stablecoin to the more theoretical about what this means for the broader financial services industry.

How do banks react and/or utilize FiUSD? Is it competitive or complementary?

- This is the big question everyone seems to be asking since the going assumption was that banks and asset managers themselves were going to launch stablecoins. That will likely still be the case, so how will FiUSD fit in? It will come down to how easy it is to move between (i.e., swap) different stablecoins. If I can easily swap between the BofA stablecoin and the Chase stablecoin, why do I need the FiUSD stablecoin as an intermediary? If that swap is not so easy to do, maybe FiUSD has value as an intermediary.

- My very loosely held hypothesis is that we end up in a world where the top ten banks issue their own stablecoins or issue one via a consortium. In that scenario, the thousands of other US banks will have the option to use those top bank stablecoins, or use something like FiUSD assuming Fiserv makes it easy for all these banks to support FiUSD out of the box. I’m skeptical that we end up with thousands of stablecoins with each community bank with 3 branches somewhere issuing a stablecoin.

Will this actually help community and regional banks adopt stablecoins?

- My sense is that we’re still a few years away from being able to walk into a community bank in the middle of America and open a stablecoin account. With that said, when you zoom out and simply view stablecoins as another way to do international funds transfer, it makes sense as an add on feature that Fiserv can sell as part of its core banking package. Adirondack Bank in upstate New York may never be able to compete with the FX desk at JPMorgan Chase (nor does it really have a need to), but stablecoins could offer a more efficient way to move funds internationally for Adirondack Bank when the need arises.

Is Fiserv going to become a stablecoin issuance platform? Will they be competitive to Zero Hash, Paxos, Brale, Bridge, etc.?

- To my understanding, Fiserv is going to be leaning on Paxos and Circle’s technology to actually issue the stablecoin. I do think Fiserv as a stablecoin issuance platform for regulated financial institutions is an interesting concept though.

How does FiUSD fit into the broader merchant services businesses?

- When you look at which the business lines within Fiserv, their high growth engine seems to be on the payments side.

- In particular, Clover is the crown jewel of their payments portfolio. I am sure the Fiserv team is thoroughly thinking through how stablecoins can enhance the Clover product. These businesses could have a need for an international payment rail like stablecoins.

Who does Fiserv acquire in the stablecoin space?

- They have a history of growing through acquisitions. They like to make strategic investments and then follow-on with an acquisition once a POC has been run. This is what happened with Finxact.

- I think there are two areas where Fiserv could likely make an acquisition. The first would be a stablecoin issuance platform (think ZeroHash, Paxos, Brale, etc.), which would be similar to Stripe’s acquisition of Bridge. The second area I could see them making an acquisition is on the stablecoin merchant acceptance side. How do you make it easier for merchants to accept and then manage stablecoin payments, particularly as these merchants look to expand globally?

Is the partnership with PayPal and MasterCard a meaningful first step in demonstrating how the payments world will deal with a multi-stablecoin reality?

- I could see a merchant getting paid in USD but then the bank wants to swap from PYUSD into FiUSD. Maybe this doesn’t matter though if both of the se stablecoins are US regulated stablecoins with the same risk rating.

- I will be watching this one closely because it gets at the heart of one of the challenges in stablecoins, which is what do we do when everyone is issuing stablecoins. Do consumers and businesses really care about the underlying stablecoin they are using? Interoperability is a big issue.

Who gets to write the roadmap for the future of tokenized deposits?

- It was assumed that banks themselves would tokenize deposits and potentially have a shared ledger, but what if the tokenization happens at the core banking level. There is an added benefit to being on the Fiserv Core if it makes it easier to settle funds between banking institutions instantly (even internationally).

Final thoughts

Fiserv taking a leap into the stablecoin space is a great sign for further adoption of stablecoins. Unlike past cycles where we saw a lot of large institutions spin up digital asset teams, which drafted up a few PowerPoint decks and scoping documents, it does feel like rubber is actually hitting the road. Institutions are experimenting on chain and somewhat quickly putting products into market to test the waters. That should excite everyone who works in this space.

Leave a comment