Stablecoins are disrupting traditional payments. Stablecoins have found product market fit. Stablecoins are crypto’s killer use case. Stablecoins are “room-temperature superconductors.”

Get a couple crypto bros in a room, and I guarantee you hear some version of this narrative around stablecoins. Ask someone to explain how this great disruption is going to occur, and it becomes more hand-wavy and harder to follow. That doesn’t mean the statements above aren’t true (I happen to think they very much are); it’s just that most, including myself, have been struggling to explain how this great disruption is going to happen. There are a lot of layers and potential ways that stablecoins can disrupt the traditional payments ecosystem, but one clear one in my mind is fund settlement. I wanted to briefly lay out how this could play out.

How does money move today?

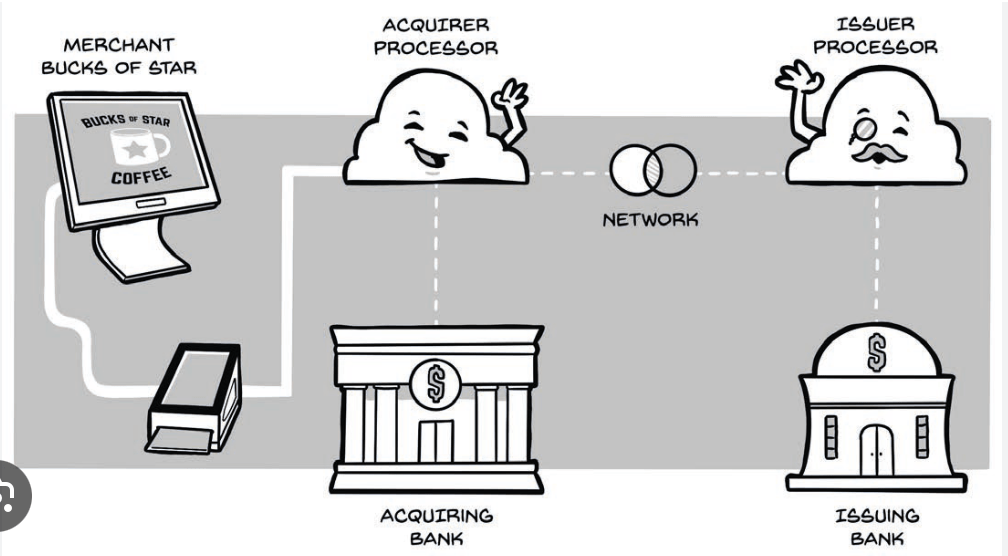

Let’s start with the traditional four party credit card model. There is a common misconception that the card networks like Visa and MasterCard actually move money. They do not. They are a communication layer, not a money movement layer. Obviously Visa and MasterCard now have many facets to their businesses, but at the core, there is a standard messaging protocol that they developed allowing banks and other financial institutions to essentially speak to each in the same language when it comes to understanding the components of a payment. For example, who is sending the money, who is receiving it, how much, etc. It sounds simple, but having one common communication layer is why I can run around the world swiping my credit card wherever I see a Visa logo.

The actual money movement side, or settlement layer, is a bit messier with many more parties involved. In the four party model, you have a merchant, an issuing bank, an acquiring bank, and the card network (i.e., the communication layer). There are actually other parties in the mix, but for simplicity, settlement is occurring between the issuing bank and the acquiring bank. At the end of the day, the issuing and acquiring bank settle up. Customers at the issuing bank spent $100,000 today, so that $100,000 is sent via ACH or wire to the acquiring bank so that it can credit its merchants for the sales they made that day. I’m way oversimplifying it, but that’s the gist. As the astute reader will know, the end merchant doesn’t actually see the funds hit their bank account until a day or two later, sometimes more. Settlement still runs as part of a batch process between financial institutions. It can be slow, and it is also costly because everyone needs to take a little cut along the way.

Image credit: Ahmed Siddiqui – The Anatomy of the Swipe

Where stablecoins fit in?

Stabelcoins are disruptive because they have the potential to upend the settlement layer. While they could also disrupt the communication layer, I don’t think we’re quite there yet although Circle’s new payment network is moving in that direction.

If I were a merchant, why would I deal with this whole process of batching payments and settling via multiple financial institutions if funds are able to move directly from A to B (i.e., from a consumer to a merchant) at the time the transaction takes place. This is of course what stablecoins promise to do and are already starting to be used for in some scenarios.

As Visa and Mastercard and others look at stablecoins, they are trying to focus on the value they can continue to add to the stack. The communication layer is super critical, and it’s hard to build networks where everyone speaks the same language. As a result, we seem to be moving into a world where stablecoins are being blended into existing payment networks and processes. While some, like Airwallex’s CEO Jack Zhang, have questioned if stablecoins really are a superior settlement layer in all corridors for moving money, Stripe is making bold moves signaling that they are going to be crucial to how money moves around the world.

This interview with Ryan McInerney does a great job of sketching where Visa plays in this. Obviously Visa sees the stablecoin threat and needs to make sure they’re positioned to survive and ideally thrive in this evolving payments environment. To his credit. McInerney talks about how Visa’s strength remains in its network and the trust its built as a mode of payment acceptance. The underlying settlement layer may change, but Visa could very well remain a critical piece of the communication layer.

There are still a lot of questions to be answered, but it’s exciting times to be building in this space.

Leave a comment