For anyone in the crypto industry interested in stablecoins, this podcast from Nic Carter and the crew at Castle Island Ventures (CIV) is a must listen. Regardless of what you like or dislike about Tether, it was a really interesting conversation about the increasingly prominent place Tether is playing in global commerce.

On March 26th, CIV aired Carter’s conversation with Tether CEO Paolo Ardoino. Here is a link to the podcast: https://castleisland.libsyn.com/paolo-ardoino-tether-on-stablecoin-bills-pursuing-an-audit-and-getting-to-400m-users-ep606

Carter mentions at the top that he had interviewed Ardoinio 5 years ago. It’s kind of crazy that I remember listening to that podcast while walking to a business school class and trying to slowly wrap my head around what crypto was all about. In that time, Tether (USDT) has gone from less than $10B in circulation to over $140B. The Tether brand (and balance sheet) has also never been strong than at this moment in early 2025. The company faces a variety of challenges, particularly in Europe, but it has solidified its hold on stablecoin payment flows across much of the world.

In general, I thought Carter did a good job of asking solid questions and pushing Ardoino a few times for more clarification on particular data points (like the user count). There were two points from this conversation that I found particular noteworthy.

First, Tether has 400M users. That’s a massive number. To put that in perspective, large banks in the US (think Chase, Wells Fargo, Citi, BofA, etc.) have somewhere in the range of 50-100M retail users. Of course, among these 400M users there is likely a very, very long tail of minimal usage, but it’s a powerful data point nonetheless. Philip Gradwell (Tether’s Head of Economics) put out a piece (and LinkedIn post) a couple months back detailing a bit more of their methodology around counting users, but this is an area I’d like to dig into more. It seems that activity on centralized exchanges is what really drives that user count (comprising about 300M of the users vs. 100M interacting with USDT via on-chain addresses).

To Ardoino’s credit, he seems to always bring the conversation back to the real-world use-cases of USDT. He talks about how it is used in emerging markets and is providing access to unbanked or underbanked populations in Latin America and Africa. It’s the part of the crypto story we should be spending more time on and forget about the memecoins.

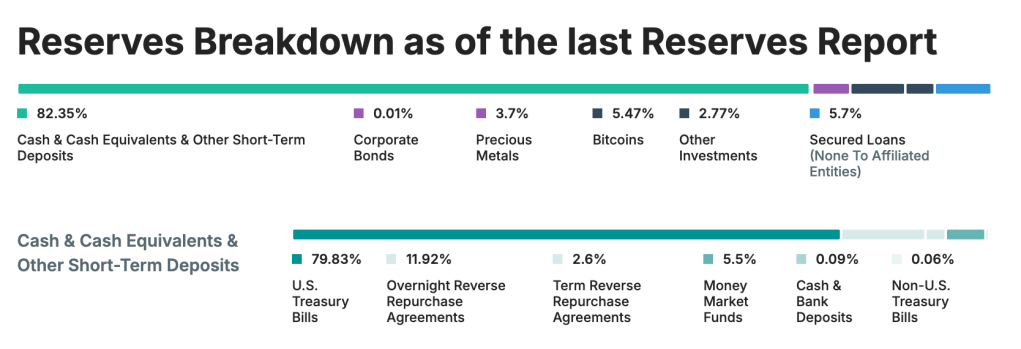

Second, Ardoino has an interesting take on Europe’s Markets in Crypto-Assets (MiCA) stablecoin regulation. He takes issue with MiCA’s reserve requirements. MiCA requires stablecoin issuers to hold somewhere between 30-60% of the underlying assets backing the stablecoin in cash at financial institutions. For the largest issuers, of which USDT would be one, the rate is 60%. This means that 60% of Tether’s underlying assets would need to be cash sitting at banks. On the face of it, that sounds fine, but that would actually be a dramatic change from USDT’s current balance sheet. For what it’s worth, USDC also has about 80% of its reserves outside of the banking system in the Circle Reserve Fund at BlackRock.

You can see USDT’s current reserve breakdown below. Almost 80% of assets are in US treasury bills and less than 0.1% is actually in cash. Treasury bills are certainly a very safe asset, and I think Ardoino would argue an ever safer asset than bank deposits during a crisis (see my last post about Circle).

As the US crafts its own stablecoin legislation, I look forward to seeing more discussions around the optimal (i.e., safest) reserve setup. I do think it is a valid point that we need to be thinking about the underlying bank stability request as governments mandate certain cash allocations. At the same time, governments will certainly have their own national interests in promoting the purchases of their own debt. Tether is now the 7th largest purchaser of US treasuries. As China and the BRICS pull back from buying US debt, Tether’s position there is likely to increase.

Leave a comment