With all the euphoria around stablecoins as of late, I would like to see more conversations about the risk frameworks that emerging stablecoins are employing. In the US, we of course need stablecoin legislation that will formerly define what a stablecoin is and set the rules of the road. The underlying assets that provide stablecoins with their inherent value are not all created equal, and there needs to be mechanisms in place to offer more visibility into the risk of the underlying assets.

Although it feels like an eternity ago, Circle’s USDC was devalued in March of 2023 when USDC holders began to worry about the viability of the 8 banks that held Circle’s cash. With Silicon Valley Bank, First Republic, and Signature Bank seeing massive outflows, holders worried about whether or not the billions of dollars that Circle held in those institutions would be lost. At the time, there was about $40B of USDC in Circulation, and 8% (or $3.3B) of Circle’s total reserves were sitting at Silicon Valley Bank (source).

The fact that USDC ran into a de-pegging issue was somewhat ironic, given that for years there had been concern over USDT’s stability and underlying assets. Everyone in the industry was always worried about USDT, not USDC. It had always been a little hazy as to where those USDT assets were held, but with Circle, you knew what you got. The money was in US banks and treasuries, usually a very sure bet, but in March 2023, that proved to be a liability.

In the last several months, the crypto industry’s relationships to US banks has changed and become less adversarial. It is still quite cumbersome to open a bank account as a crypto startup, but it is not as onerous as it was in 2023 and 2024. Back in 2023, Circle had 8 banking relationships. While it is not publicly disclosed, I assume they only had 8 bank relationships because it was relatively hard to convince traditional banks to set up accounts for them. These seem to be the 8 banks they were using at the time:

- Citizens Trust Bank

- Customers Bank

- New York Community Bank

- Signature Bank

- Silicon Valley Bank

- Silvergate Bank

- US Bancorp

- BNY Mellon

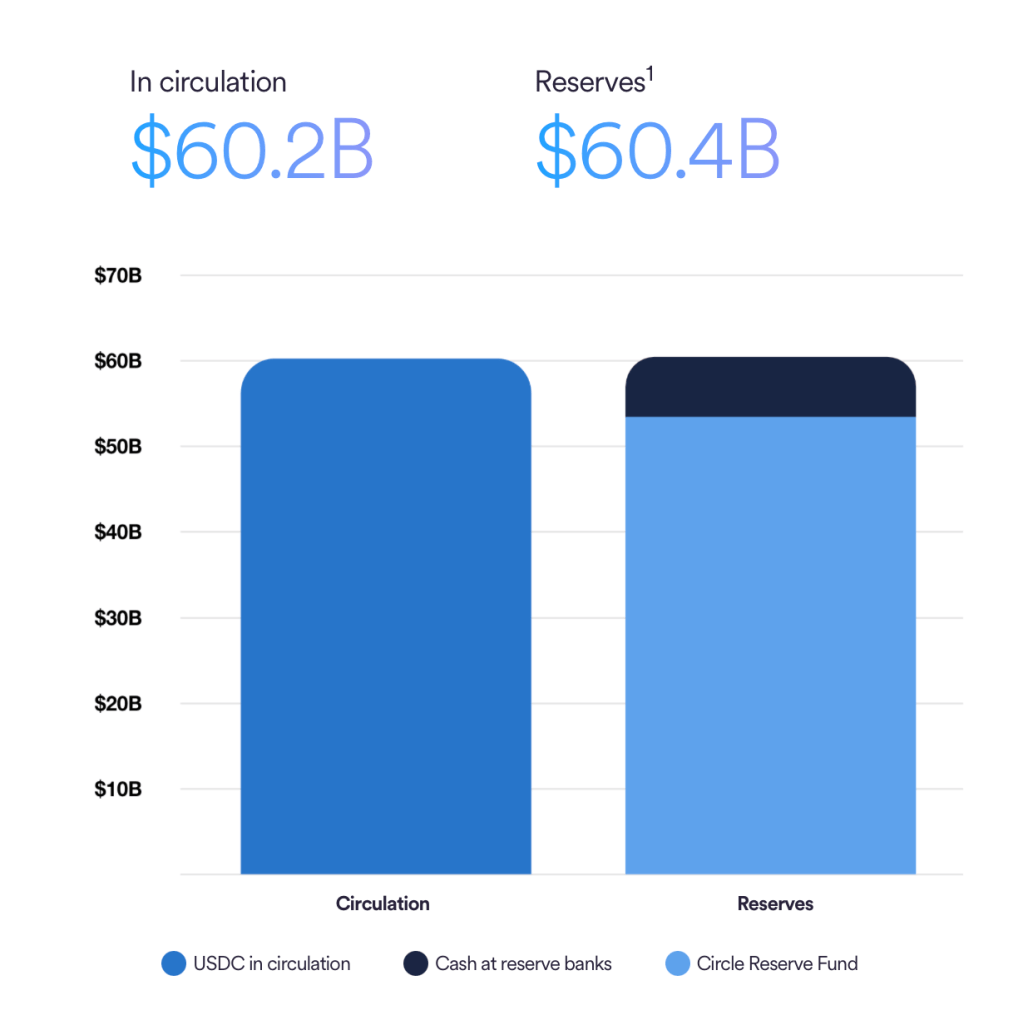

As I was poking around the Circle website the other day, I noticed in their disclosures that they now hold most of their cash at a GSIB bank (Globally Systemically Important Bank). An important note here is that cash makes up about 12% of the reserves (~$7B now) while the remainder is in the “Circle Reserve Fund.” This reserve fund is a mix of US treasuries and some other short-duration assets.

We’ll put the Circle Reserve Fund on the side for now. That deserves a whole other post to discuss. If you are interested though, here is what the composition of the reserve fund looks like.

For now, I’m interested in this $7B in cash held in the banking system. Within there voluntary disclosures, Circle discusses how it has taken steps to ensure it avoids a repeat of 2023.

Following multiple recent bank failures, Circle has taken steps to reduce risk from the banking system by now holding substantially all of the cash portion of the reserve at one of the world’s 30 global systemically important banks, also known as a GSIB.

Given Circle had an existing relationship with BNY Mellon, we can assume the GSIB they use is BNY Mellon. I have also seen articles though that Circle uses Standard Chartered Bank, so I imagine they have been able to diversify their banking relationships, particularly internationally in the last year. I assume this is a core tenet of the Circle risk management team. Even if the majority of the cash sits in a GSIB like BNY Mellon, they would likely want ever further diversification across a range of global institutions. In my mind, this is one of the biggest issues that is not discussed enough in the stablecoin conversations – which banks are actually holding the cash? We’re seeing more voluntary disclosures, but it would be great to see more clarity around this.

It’s interesting when you think about this in the context of MiCA stablecoin regulation in Europe. MiCA requires anywhere from 30-60% of the reserves to be held in cash deposits at a credit institution in Europe. USDC has 12% of its reserves in cash at banks, so this has actually a question I’ve started digging into to better understand how Circle maintains its MiCA compliance without having a higher cash reserve basis. It seems it has to do with USDC not being fully issued out of Europe whereas their EURC stablecoin is (Patrick Hansen post). As the US works towards its own stablecoin legislation, it will be interesting to see where it lands in terms of these cash requirements and how stablecoins address any underlying stability risks from the banking system.

On a separate note, one of the most interesting statements in this disclosure article from Circle is that they ultimately hope to maintain funds at the US Federal Reserve. Presumably there would be no safer place to leave your deposits. While it is very unlikely the US ends up with a CBDC at this point, particularly given the current administration’s dislike of the concept, such an action would seem to make USDC fairly close to a US CBDC.

We have always aspired to hold the cash portion of the USDC reserve directly with the Federal Reserve, fulfilling our vision of USDC as true tokenized cash. To do so will require stablecoin legislation.

There is certainly more to come on this topic as stablecoin legislation makes its way through the US Congress in the coming months.

Leave a comment