Introduction

A recurring critique thrown at crypto is that it is a technology in search of a problem. In the typical back and forth that then ensues over the value of crypto, the topic of remittances inevitably comes up. It’s a use case that many are familiar with and have personally felt the pain of. Sending money between countries is inefficient and expensive.

As I dug into this topic, I found that a major research gap exists in terms of tracking just how much remittance volume is flowing via crypto rails. Of course, I am not a research expert and have a day job, which prevented me from combing every possible report, but there are very few sources available that even take a pass at triangulating the crypto remittance volume.

Crypto, and stablecoins in particular, are a new technology at the beginning of the adoption curve, but I was still shocked at how difficult it was to find studies or reporting around remittance volumes in crypto. Don’t despair though, I was able to come up with a rough estimate after a little digging and employing some consultant math. 😁

Setting the scene

Let’s start by setting the scene. The Global Migration Data Analysis Centre (GMDAC) estimates that USD 857 billion of remittances were sent in 2023. After a dip in 2020 during COVID, remittances have been steadily growing year after year and are expected to grow at a rate of 3% in 2024. India is the largest receiver of remittances with $89B received in 2023 with Mexico and China not too far behind.

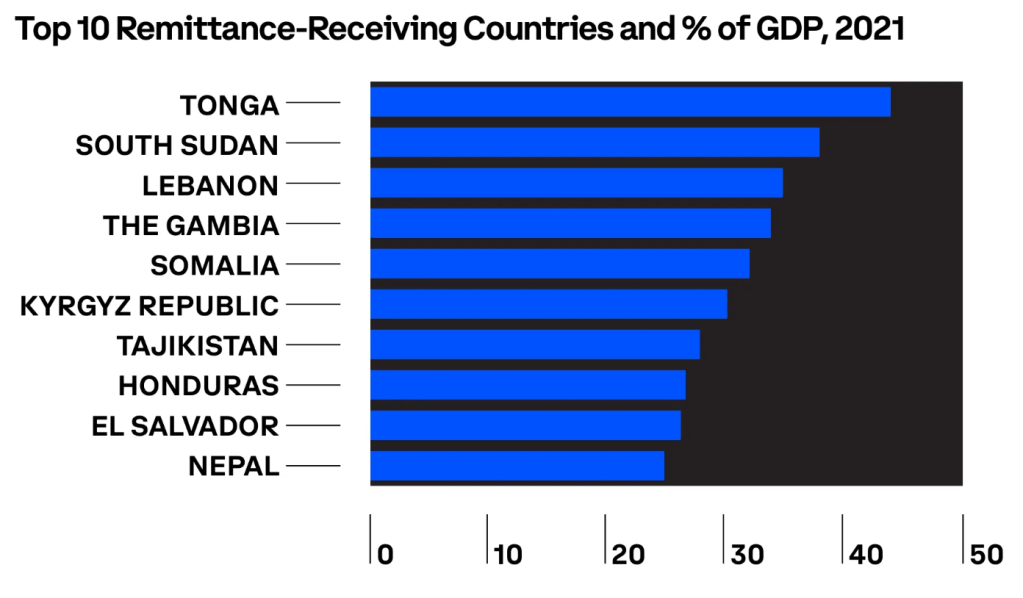

Not surprisingly, $857B is a lot of money. Remittances are a big deal and in some countries make up a significant portion of GDP. India is obviously one of the world’s largest economies at $3.57T, so while the $89B of incoming remittances is absolutely significant and life-changing for many families, it only represents ~2% of India’s GDP. For much smaller economies though, remittance flows can account for over 20% of GDP. The chart below shows the countries where remittances account for the largest share of national GDP.

The fee problem

We’ve established that remittances are large and extremely significant for many economies, so let’s understand more about transfer fees and just how much money is being lost to intermediaries in this process. The GMDAC estimates that the average cost of sending USD 200 is 6.4% (~$13)! This cost varies by region and method used for transfer. Asia tends to have the lowest remittance costs at 5.8% while Sub-Saharan Africa sees an average cost of 7.9% 😱. The Sustainable Development Goals (SDGs) from the United Nations set a target of having the global average remittance fee be only 3% by 2030. Unfortunately, we’re a far way off from this.

When you start digging into the channels used to send remittances, you see a massive difference in fees depending on the method used to send funds. The chart below shows how much fees vary by remittance service provider (RSP). As you can see, that orange line for the banking channel sits well above the other providers with an average of over 12% for remittance transfers via banks. Fortunately, there are a variety of new digital channels emerging, but the traditional method of using a bank to send funds remains exorbitantly expensive.

If you want to dig deeper into average cost data by region, the World Bank puts out a comprehensive quarterly report on remittance costs all over the world and by channel used to send the money. In the next section, I want to dig more into the mechanics of why these fees are so high and also why it takes so long for money to travel from A to B.

The intermediary problem

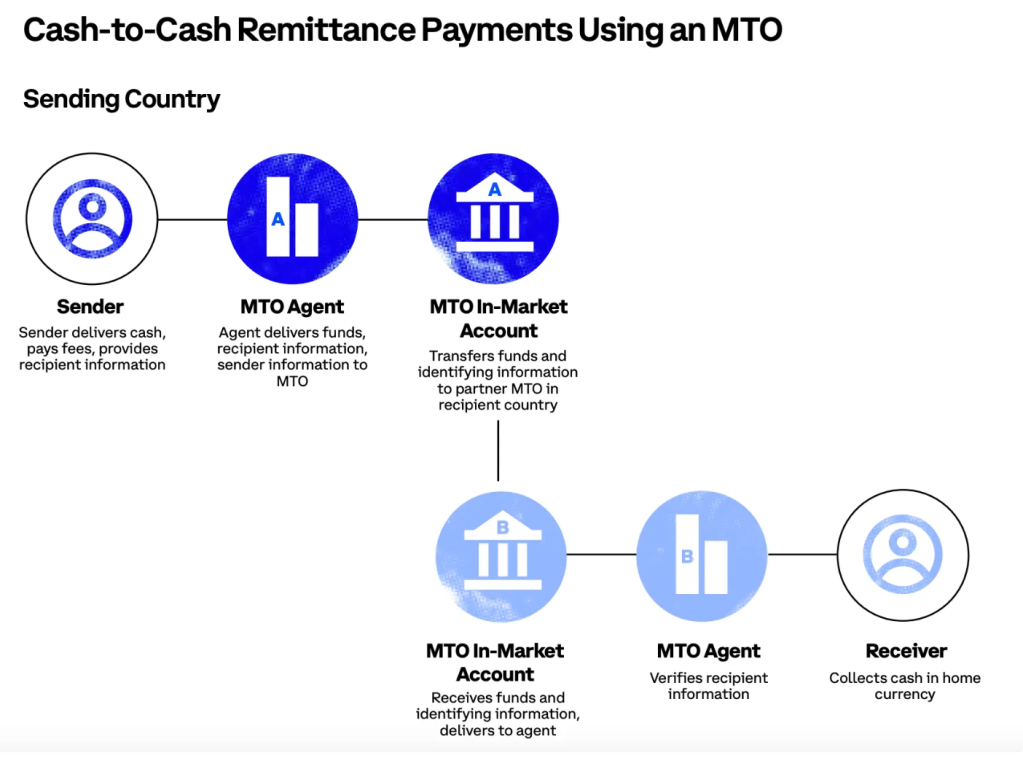

As discussed above, there are several different channels used for sending remittances. I could write a whole other article on the different transfer methods, but at a high level, some version of the graphic below occurs (thanks to the Coinbase Institute for the graphics). Let’s take the example of a person in the United States who sends funds to Mexico. In the simplest example, a person takes some cash she’s earned in the US, goes to a money transfer agent in New York City, and then that money is sent on its way via the agent’s network. Depending on where the funds are going, that money might stay within the agent’s existing network or hop between several banks. The recipient eventually heads to their own local agent in Mexico and takes cash out.

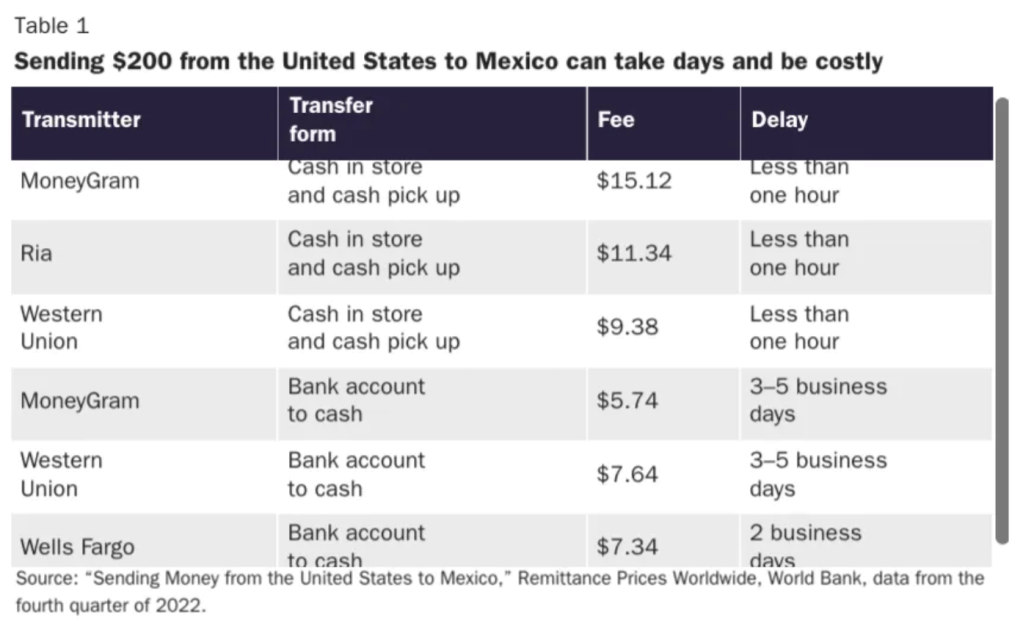

The example is simple enough, but depending on all the various permutations of services available, that simple transfer will have likely incurred a significant fee and could arrive within an hour or within 5 days! This chart below does a great job mapping all the permutations of fees and transmission times by method.

The proliferation of digital wallets and smartphone technology in the last decade has already begun to change the game and bring down fees. We are already better off in that digital wallets remove the need to physically take some cash somewhere and then have multiple intermediaries move that cash across the globe to another end point where someone takes out cash. Digital wallets in themselves are not a perfect solution, but they are a step in the right direction. The other massive issue is the existence of all these intermediaries, even when a digital wallet is used. This is where crypto comes in.

How does crypto solve this?

The ways in which crypto can solve the challenges faced with remittances have been well documented and written about extensively. It’s fairly straightforward; you go from a transaction that sometimes touches 3 or more intermediaries to one where both the sender and the receiver can be on the same network with no need for an intermediary. As the graphic below illustrates, you simply need two individuals with wallets on the same network (and even that is becoming less important with cross-chain swapping capabilities).

We have mostly been discussing the fees associated with remittances, but the timing is another point of friction and frustration. As the table above from the Cato Institute showed, it can take anywhere from a few hours to a few days for funds to actually clear. With just about every EVM chain and Solana, money moves in mere seconds. It’s a massive improvement, and there is no doubt that in the years to come that near instant fund movement will become the standard, not the exception.

Crypto might play such a big role that the very idea of a remittance will become an anachronism. As former Coinbase UK CEO and MoonPay’s Chief Growth Officer Zeeshan Feroz argues, remittances are an “artefact of our current financial system.”

How much remittance volume is flowing through crypto today?

A lot of ink has been spilled on the game-changing potential of crypto for remittances, but for many years, the volatility of crypto prices were a major hindrance to cross-border transactions and the broader use of crypto for payments. The massive uptake in stablecoins, especially with USDT and USDC, over the last 5 years has removed that challenge. Now that stablecoin products have been in the market for a couple years, it feels like we are well-placed to start digging into the role crypto rails are actually playing in remittances, not just the hypothetical.

As I mentioned at the top, it was challenging to find an answer to the question of how much remittance volume runs on crypto rails. I imagined this would be readily available information, but I really had to dig to come up with an estimate. In the end, the best approach I could come up with was zeroing in on the US-Mexico exchange corridor and then extrapolating out a rough estimate for what global remittance volumes in crypto might be today.

In 2023, $63B in remittances flowed from the US to Mexico. With this fact in mind, I tried to find any data around how much crypto volume flowed from the US to Mexico to get a sense for how that compared to the $63B. When it comes to centralized crypto exchanges, Mexico has a highly concentrated market. Bitso is the clear market leader with one estimate stating that they control 99.5% of all trading volume among CEXs in the country. Binance and Bitfinex have a presence, but their volumes are minuscule.

In 2023, an article from Fast Company (cited by the Crypto Council for Innovation) noted that Bitso processed $4.3B in transactions that would qualify as remittances from users who sent money from the US to Mexico. It’s a little unclear whether Bitso’s volumes are included in that national remittance figure of $63B, so I am going to assume they are not, taking a more conservative approach to estimating crypto’s share.

Of course, I haven’t taken into account direct wallet to wallet transfers. A person with a Metamask wallet in the US could simply send USDC to their family member in Mexico who also has a Metamask wallet. The Mexican family member may eventually cash out of crypto to Mexican Pesos using Bitso, but Bitso would not be able to track that as a remittance payment. These types of wallet to wallet transfers are obviously extremely difficult to track at the moment. Although volume on decentralized exchanges has been roughly equal to that on centralized exchanges, I would imagine that remittance flows are more likely to occur via centralized exchanges where it is easier to set up an account and abstract away the complexity of crypto, especially for populations that might be less technologically savvy. With that said, there is definitely significant value flow occurring here via this channel, so I think it’s fair to round up that $4.3B to $5B to account for direct wallet sends and more informal crypto exchanges.

You may have heard of companies like Félix Pago that are enabling remittance payments via WhatsApp and USDC. It’s a great solution that is hyper-focused on simplifying the user experience where both parties have no need to know about the crypto rails underneath. Players like Félix Pago use Bitso to move funds, so they are included in that total transfer number from Bitso above.

So all in all, we’re roughly estimating that there are $5B in crypto remittance payments into Mexico from the US. We add this $5B to the $63B in remittances from existing remittance channels like banks, Western Union, etc., and we land at $68B. That means crypto accounts for about 7% of all remittance flows into Mexico. Not bad! There are certainly a lot of caveats, asterisks, and unknowns around that number, but it doesn’t sound crazy.

Can we extrapolate that 7% globally? Maybe…

Mexico and Latin America in general tend to be a bit more crypto savvy than most other emerging markets. Latin American governments have been somewhat friendlier to crypto whereas governments like India have gone back and forth on outright banning crypto or taxing all crypto transactions at exorbitantly high rates. Reporting from Bloomberg notes that crypto accounted for 10% of the $5B in remittances that flowed into Venezuela, so this data point does help as a sense check for the 7% we estimated for Mexico.

Although I have not been able to find any data on crypto remittances for India, my gut is that crypto remittance volume into India is going to be lower than 7% just given the complexities of transacting in crypto as an Indian citizen. On the other hand, Nigeria may see more remittance volume in crypto given its citizens’ proclivity to hold crypto as noted in the new stablecoin report from Castle Island Ventures and Brevon Howard. All in all, estimating that 7% of all remittance volume occurs in crypto is a very rough guess, but it does give us a starting point and would mean that about $60B a year is flowing in crypto remittances.

Conclusion

Ultimately, this exercise highlights the need for more robust data and reporting on the role that crypto is playing in streamlining and lowering the cost of remittance flows. If crypto can play a significant role in helping the world achieve the Sustainable Development Goals’ target of 3% remittance fees (or lower) that will be a major win impacting the lives of hundreds of millions of people. Looking at metrics like total stablecoins minted and total value locked for different protocols is great, but we need to find more robust ways to understand what tokens are used for. There is of course a penchant for privacy in the crypto ecosystem, but that shouldn’t hold us back from understanding and demonstrating real-world use cases.

In the end, crypto should be a means to an end. We need to move money faster with lower fees, and crypto appears to be the best technology around to do that. I’d like to end with a quote from Manuel Godoy, the leader of Félix, one of the many companies tackling this remittance problem head on.

“Crypto is a powerful enabler for remittances, but you have to abstract that from the user. The user doesn’t care about that. I always say that it could be a donkey crossing the border, it doesn’t matter. What they want is the money, the local currency and they want it instantly at the best possible price. And crypto enables that on the back end.” – Manuel Godoy, CEO of Félix (source)

More resources

If you would like to read more, here are some of the resources that I drew on when writing this piece.

- Crypto Council for Innovation – 10 facts about remittances and crypto

- World Bank – Remittance Prices Worldwide Quarterly Report

- PYMNTS and Stellar Development Foundation collaborated on what seems to me to be one of the most comprehensive survey conducted so far on how crypto fits into payment methods being used for cross-border payments. The challenge is that the report is a little dated no from September 2021.

- Fast Company article on Bitso who processed $4.3B in remittances between the US and Mexico in 2023.

- Coinbase Institute – “Crypto and Remittances”

- Moonpay article on the potential role of crypto for remittances

- Cato Institute – “Money Across Borders”

Leave a comment