Introduction

In the world of cryptocurrency, 2020 has become the year of the stablecoin. Stablecoins can be broadly defined as a “…class of cryptocurrencies that attempts to offer price stability and are backed by a reserve asset.” In most cases, stablecoins are pegged to the value of the dollar (the “reserve asset” mentioned in the preceding definition). I’ll get into a taxonomy of the different types of stablecoins below; however, before that, I want to give some context.

Context

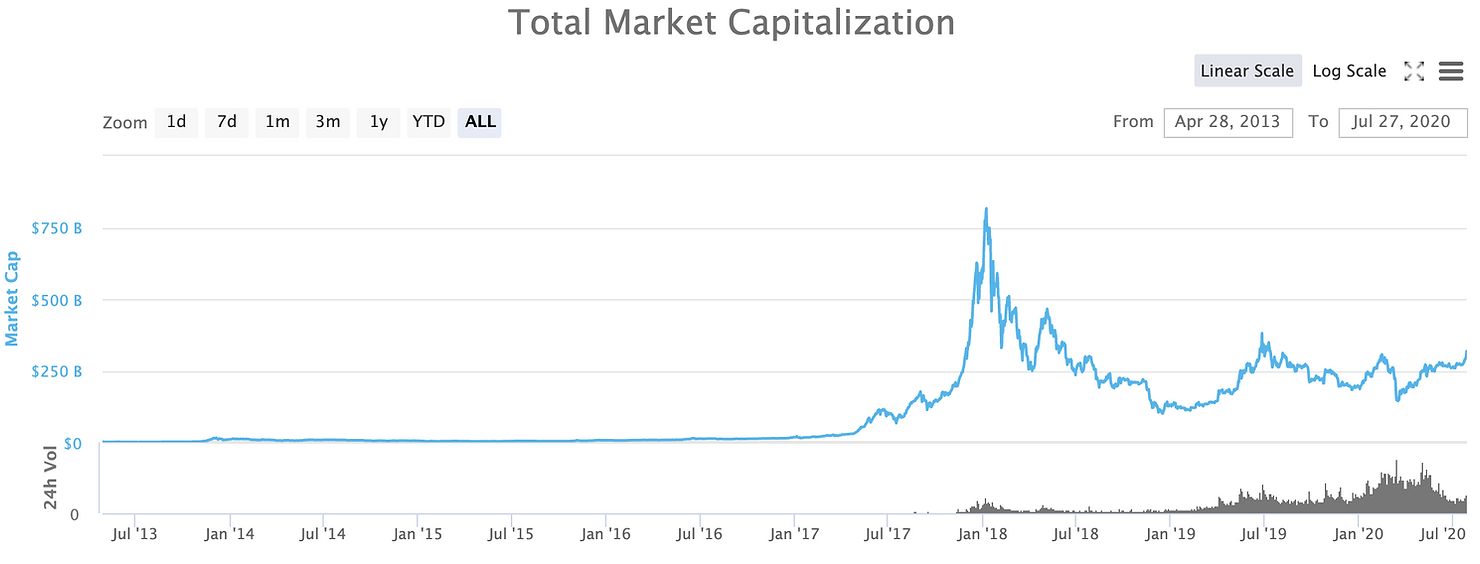

The total value of issued crypto-currency fluctuates quite a bit, but in the first half of 2020, it has been in the ballpark of $250B. As of July 17th, it was ~$270B. When one considers that mutual funds and ETFs are each multi-trillion dollar industries, crypto as an asset class is still tiny, but it punches above its weight in media attention and investor interest. The most recent example of this has been the admission by hedge fund investor Paul Tudor Jones that he has 2% of his portfolio allocated to Bitcoin.

In the graphs below (sourced from CoinMarketCap), you’ll see the crazy pop in the crypto market cap to over $750B in late 2017. This was during the initial coin offering (ICO) craze where people were issuing coins for a variety of weird projects, most of which have proven worthless and many are now being investigated by the SEC. Ignoring the 2017 spike, you’ll notice two things. First, Graph 1 shows that over the last two years the market cap has roughly stabilized around $250B.

Graph 1

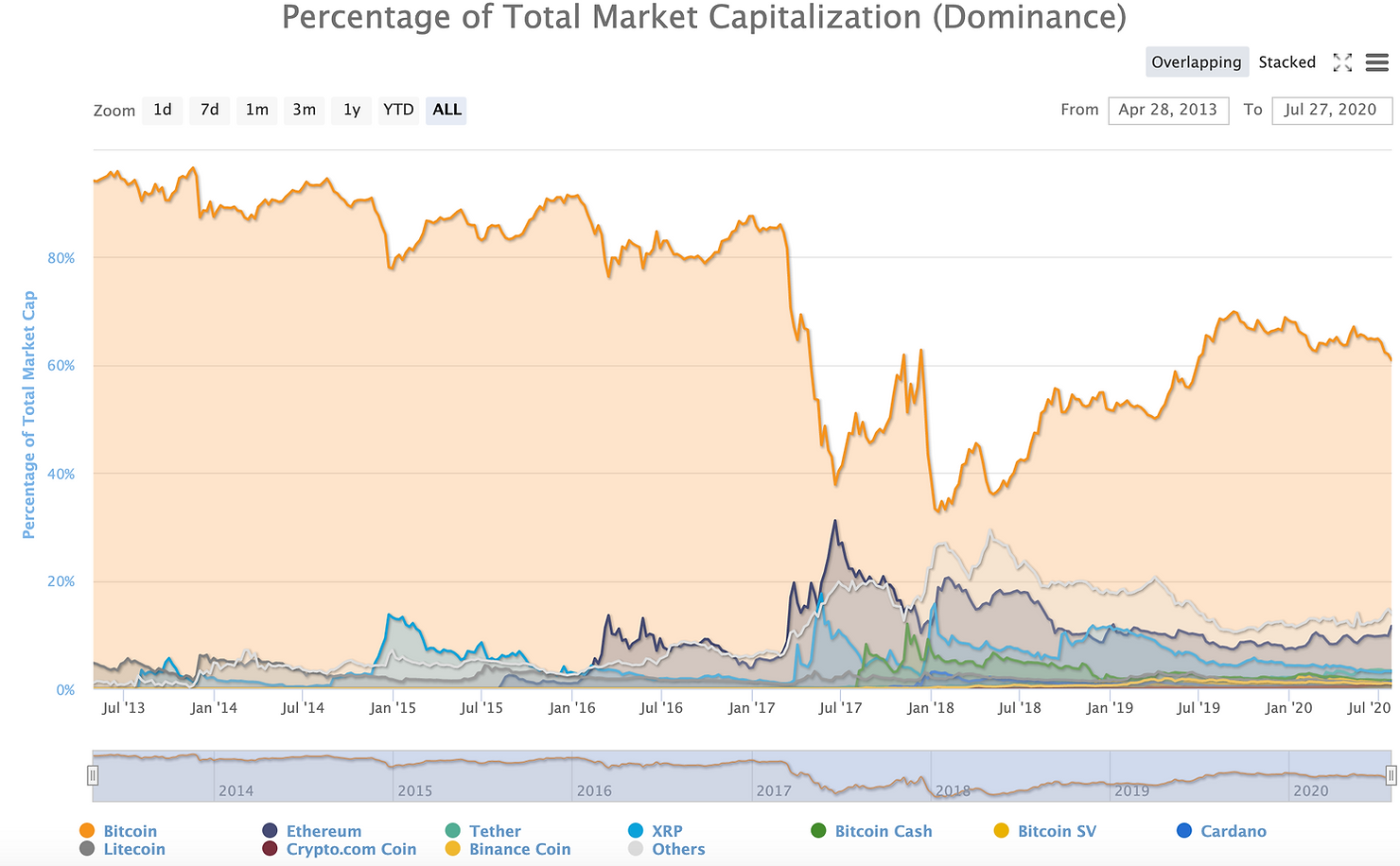

Second, Graph 2 breaks down the composition of this $250B in value revealing that Bitcoin (shaded in orange) has historically been the primary driver of value. This is no shock given that Bitcoin was the first, is well known, and has arguably gained a use-case as a store of value acting like digital gold.

Graph 2

I mostly show these charts from CoinMarketCap because they are fun to look at, but what I really want to focus on in this post is the variety of colored lines towards the bottom of Graph 2. Bitcoin’s share of the crypto market cap remains above 60%, and it is not likely to be dislodged from its top spot anytime soon; however, there has been some reshuffling in the ranks with the rise of stablecoins. The most famous of which is Tether. This stablecoin is difficult to spot above, but Graph 3 shows you its rapid rise in the first half of 2020.

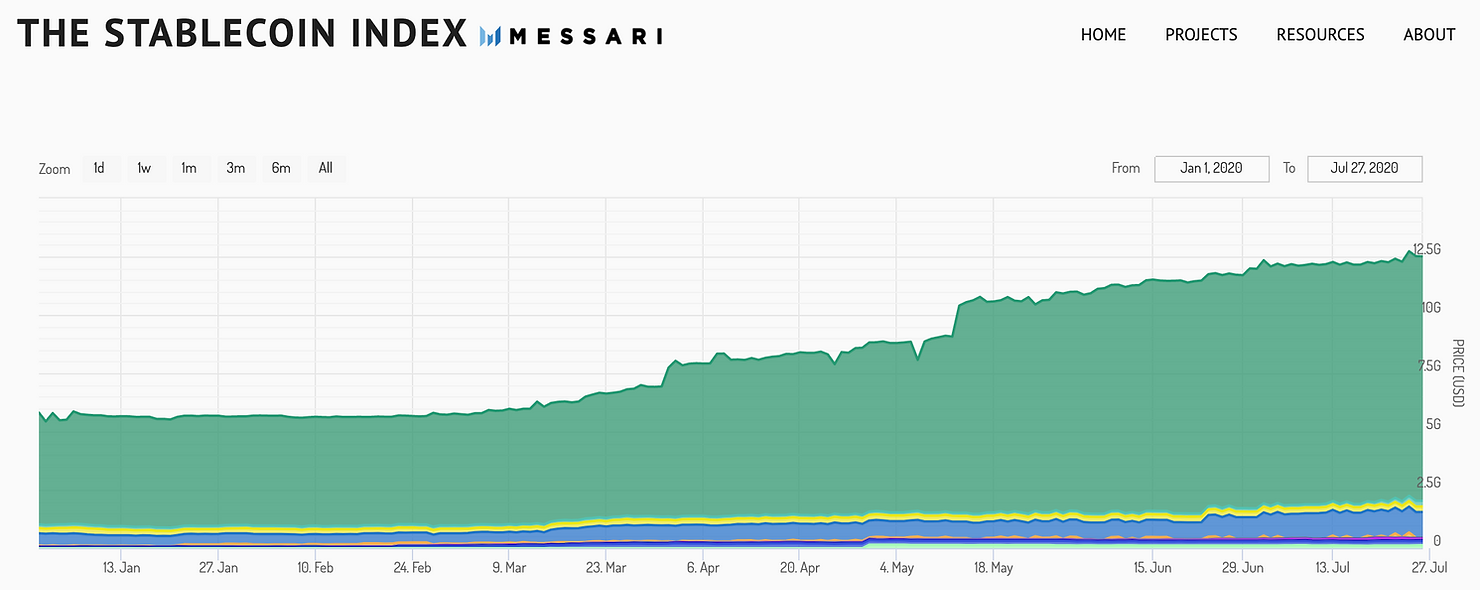

Graph 3

Start by focusing on the blue line above. That is the market cap of Tether. It has gone from less than $5B in January 2020 to about $10B today, making it the third most valuable cryptocurrency as of July 2020. It’s also interesting to take a look at that dark green line tracking the value of Tether in exchange for a US dollar. As the stated goal of Tether is to track the US dollar 1:1, it is no surprise that it roughly appears to do that, but it’s not perfect – more on that later.

Looking at Messari’s Stablecoin Index, we see that the total market cap of all stablecoins is only about $12.5B as of late July 2020. In this microcosm of the stablecoin world, we see that Tether (dark green in Graph 4) is overwhelmingly the biggest player accounting for roughly 80% of all value in stablecoins.

Graph 4

Why care about stablecoins?

So why do we care so much about stablecoins if they represent less than 5% of the crypto market cap? Crypto as an asset class is relatively small, so, again, why do we care? There are a few reasons.

1) They doubled

As the charts above make clear, the value of stablecoins has doubled in less than six months. Sure, the value doubled off a relatively small base of less than $5B, but this is still reason enough to perk up and take notice. Stablecoins are not a new innovation, at least in the short history of the crypto world. One of the first stablecoins, Tether has been around and traded since 2015, but the current spike in its usage is unprecedented.

2) They are a facilitator

One of the public faces of the Tether team, Paolo Ardoino, was recently featured on a podcast where he discussed his theory for why Tether’s market cap has exploded. Ardoino suggested that Tether is being used by traders as a way to quickly move in and out of other cryptocurrencies, like Bitcoin. Like the stock market, Bitcoin and other altcoins took massive dives in March 2020 in the midst of the COVID-19 crisis. This huge dip was a critical buying opportunity, but many investors were potentially kept on the sidelines due to the slow process of exchanging fiat currency (e.g., US dollars) for crypto. Traders need to be able to move into and out of Bitcoin quickly, and stablecoins like Tether enable that since they are on-chain assets. Many traders were caught off guard in March. As a result, one theory is that they are now loading up on stablecoins so as not to miss the next dip.

The use case for stablecoins that Ardoino articulates is nothing new, but the market volatility of the last several months seem to have made this use case all the more relevant. If you’re bullish about the space, you might see this as the next step of maturation in the evolution of the crypto trading world.

3) They are being used

One criticism of cryptocurrency, and Bitcoin, in particular, is that it is useless; it sits in a wallet and rarely moves as a mode of transaction. In one count, 60% of Bitcoins did not move in the last year. Stablecoins, particularly Tether, have been receiving a lot of attention because there is a lot of transaction volume. People are moving these things. The daily transaction volume of stablecoins is now slightly higher than that of Bitcoin. This shouldn’t necessarily be shocking because Bitcoin was never going to be a good currency for transactions given its price volatility and slow transaction processing time. With their consistent value, stablecoins are proving to be easier to transact in, leading to broader discussions about their application for international remittances and other use cases in emerging markets.

4) Facebook’s doing it

Facebook’s foray into cryptocurrency is too long of a story to tackle here, but in May 2020, Facebook released an updated Libra white paper. There were a range of changes and updates to the project, but chief among them was the further definition of how the Libra Coin would function. Instead of just one Libra Coin that could potentially challenge the monetary sovereignty of nations, the Libra Association is now creating a basket of stablecoins that will be pegged to national currencies. For example, there will be a LibraUSD and a LibraEUR. The value of the Libra Coin will be based on a weighted basket of these pegged stablecoins.

The project is still in the works and has not launched yet, but existing stablecoins give us a window into how the Libra system might function and how it could be used. With over 2B users on Facebook, the successful launch of the Libra stablecoins could have huge implications for the crypto market and the broader financial system. Libra’s launch date is uncertain, but it would likely prompt a big jump in that $12.5B stablecoin market cap.

5) More projects

This last reason perhaps dips into a bit of circular logic, but we care about stablecoins because there has been a big uptick in the number of stablecoin projects. There are now over 100 stablecoins that are either active or in development. One of the world’s most well-known venture capital firms, a16z, has made a bet in the space, and capital is flowing towards these projects. There is certainly a sense that this could be the 2017-2018 bubble all over again, but there seems to be demand for providing access to a cryptographically-secured, digital version of the dollar. As countries like Zimbabwe and Lebanon battle currency crises, some see stablecoins as the blockchain killer app that could have utility, especially in emerging markets where there is a high demand for dollars.

How do the mechanics work?

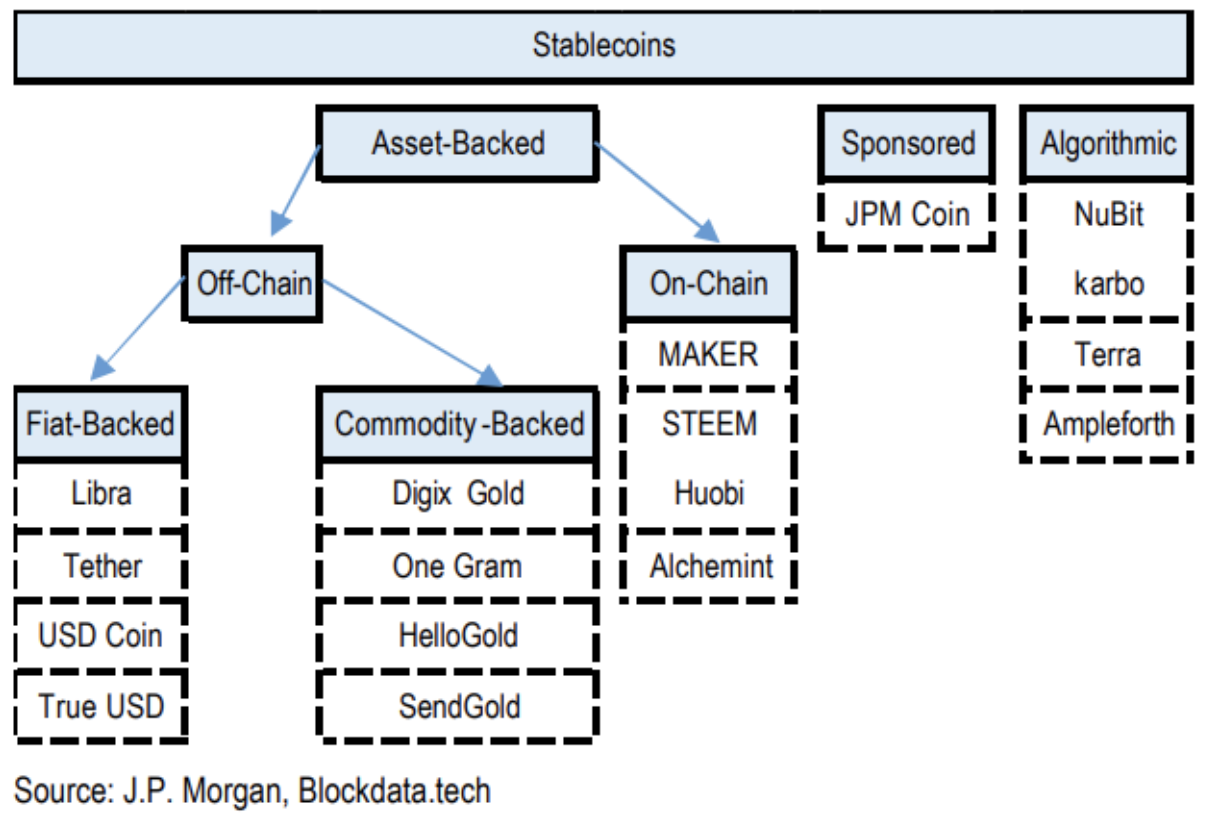

I promised above that I would spend more time on the definition of what a stablecoin is and how these things work. I’m still making my way along the learning curve myself, and given that there are over 100 projects, a standard definition is tough. The best definition and classification of projects I’ve seen so far comes from J.P. Morgan’s research team, which published a report in February 2020 entitled “Blockchain, digital currency and cryptocurrency: Moving into the mainstream?” Pages 41 through 57 dive into stablecoins with a focus on the Libra Coin. On page 43, they offer this nice little taxonomy of stablecoins.

Of course J.P. Morgan has to make its own JPM Coin look unique, so it is in its own separate “Sponsored” category, but the basic breakdown of stablecoins into “Asset-Backed” and “Algorithmic” is helpful. The overwhelming majority of stablecoin projects fall into the Asset-Backed category, and Algorithmic stablecoins have had a much harder time catching on. Rather than peg themselves to some fiat currency or commodity, Algorithmic stablecoins use a programmatic set of rules to control the creation and destruction of coins to hold the value of the currency relatively constant. It’s complicated, and that’s about as much as I understand.

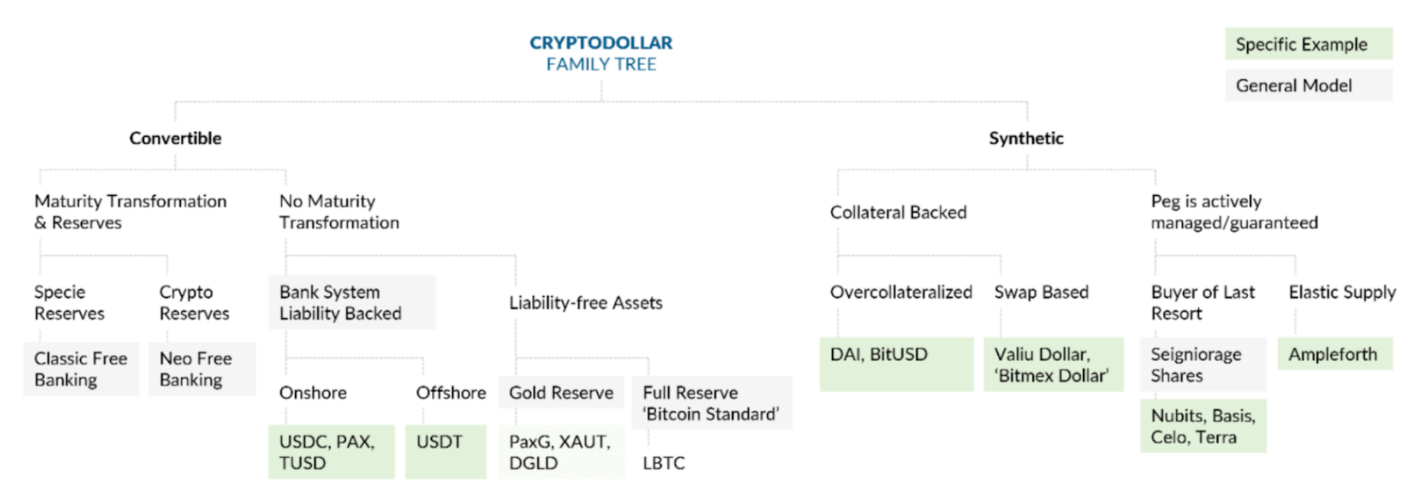

Returning to the Asset-Backed side, the asset most-used for backing is the US dollar. According to a report from Castle Island Ventures, “…96.7 percent of circulating cryptodollars by monetary base were intended to track the return of the US dollar” (page 16). This same report offers an alternative taxonomy, which is worth mentioning. Castle Island breaks down the world of stablecoins by those that can be redeemed (“Converted”) for the underlying asset which they track and those that cannot be redeemed.

Source: Castle Island Ventures stablecoin report page 16

The combination of these taxonomies gives a pretty good lay of the land. The Castle Island classification system illustrates the broad possible range of projects, but at the moment, Tether, USD Coin, and Dai are the most important in the ecosystem and illustrate the breadth of mechanisms used to create stablecoins. I briefly explain each of these three stablecoin projects below.

Tether

I’ve mentioned Tether a lot already primarily because it’s one of the original stablecoins and the most used. It was created as a “value exchange vehicle,” enabling traders to lock in gains on Bitcoin without having to convert back off-chain to a fiat currency. That is still the primary use case of Tether. The stablecoin gained initial traction in 2017 when China was limiting access to fiat on-ramps, and it has since gained popularity in the US and other markets.

Tether has courted some controversy in the last several years due to the lack of transparency around the reserves backing it up. It originally claimed that each USDT was backed by a dollar in deposits, but it has changed its tune. On its website, reserves are defined as, “…traditional currency and cash equivalents and, from time to time, may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities.” Tether Ltd. now has a page on its website posting its daily reserves, but it is still unclear from my research whether or not Tether has ever had a full external audit.

USD Coin

USD Coin (USDC) was launched in 2018 via a collaboration between Circle and Coinbase. Like Tether, USDC is pegged to the dollar at a 1:1 ratio. Although the current supply of USDC is much smaller than Tether, USDC recently crossed the $1B mark. In terms of reserves, it uses deposits with a variety of banking partners to maintain a 100% reserve ratio and has an outside party do a monthly audit on these reserves. The FAQ on the website details this stating: “When you wire fiat funds into our system, we deposit those funds with one of our banking partners. In the future, Circle may also invest these fiat funds in highly-liquid, AAA-rated fixed income securities.”

Dai

Dai is a bit different from Tether and USDC in that it is a “crypto-native” stablecoin, meaning that it does not derive its consistent value from a fiat currency or commodity off-chain. Instead, Dai uses a collateralized debt position (CDP) where users deposit Ether in exchange for Dai. The CDP functions like a margin loan but with a few more complicated features. That is a gross oversimplification of the project, but frankly, I’m still trying to wrap my head around how it works. This article from Gregory DiPrisco does a solid job simplifying the explanation of Dai as much as possible, and I would start with that if you’re curious. There is also this conversation about Dai’s uniqueness as a censorship-resistant stablecoin that is worth a read.

Lessons from history

Before closing out this post, I want to cover what I see as the most significant concern for stablecoins: defending the peg. While investigating the three most important stablecoins (Tether, USDC, and Dai), we saw that there are a variety of techniques used to keep the value of these coins relatively constant. When I first started reading about stablecoins, my biggest question was how are these coins any different from a sovereign currency like the Thai Baht, Argentinian Peso, or Hong Kong Dollar, which currently are or have been pegged to the US dollar at some point. The Hong Kong Dollar has been pegged to the US dollar since 1983, and the stability of this peg has been credited with facilitating Hong Kong’s economic growth. Unfortunately, Thailand and Argentina have each had episodes of currency crises where they were forced to abandon the peg when they could no longer defend the pegged exchange rate of their currencies.

Scrolling through Crypto Twitter and Google, I have not yet come across a satisfactory answer to my question above. My guess is that if you asked the creators of these stablecoin projects, they would tell you they’ve built mechanisms and safeguards to prevent a run on their reserves. Presumably, these mechanisms and safeguards would protect these projects from a speculative attack by investors on a stablecoin’s value.

I’m still in the process of diving into the mechanics of dollar pegs and currency boards, but it seems like one of the reasons the Hong Kong peg has been successful is due to its 100% reserve rule. While all three of the top three stablecoin projects are technically trying to maintain full reserves, USDC does seem to have taken the most conservative approach. As noted above, USDC seems to have a dollar sitting in a vault for every USDC coin out there, and there is a stated auditing process in place to verify this. Any auditing of Tether’s reserve assets is a bit more opaque, but presumably they could redeem all of the currency on fairly short notice although this has been called into question in the past. Dai is managed like a margin loan with additional safety guards in place to defend against a drop in the value of Ether.

There is clearly a need for more auditing to ensure reserves truly exist. At the same time, history offers a cautionary tale not to overcomplicate the reserve mechanism and venture into a fractional system. I hope to see more writing on this topic to better understand how stablecoin reserve mechanisms work and best practices around auditing.

If stablecoins do continue to grow in popularity, there will eventually be challenges around where Tether and others actually keep their reserves. Is JPMorgan Chase or Bank of America going to want $50B in deposits that back up Tether coins? Banks will need to consider how to treat the risk of these deposits. At the same time, the crypto community (and their auditors) will likely need to come to some agreement over how safe it is to have stablecoin reserves in the fractional banking system. There seems to be a bit of risk here that I haven’t seen much chatter about. This will be important to watch going forward.

Leave a comment